Palantir (NASDAQ: PLTR) had a blowout quarter.

For about 11 straight quarters, the company impressed the Street with strong revenue growth, and continued to increase guidance. It’s part of the reason the stock has soared more than 1,800% over the last three years. This week, the company’s EPS of 33 cents beat by five cents. Revenue of $1.63 billion, up 84.4% year over year, beat by $90 million.

Analysts were looking for adjusted EPS of $0.28 on $1.54 billion in revenue.

U.S. revenue jumped 104% year over year. U.S. commercial revenue was up 133% year over year. U.S. government revenue jumped 84% year over year.

And, as noted by CEO and co-founder Alex Karp:

“Palantir’s Rule of 40 score has soared to 145%. We have shattered the metric, a feat matched only by other fellow AI infrastructure companies: NVIDIA, Micron and SK Hynix. Momentum surged as we grew 85% last quarter – our highest-ever year-over-year growth rate – by more than doubling our U.S. business, and now we are raising our full-year revenue guidance to 71% growth, 10 points ahead of our guidance from last quarter, driven by our confidence in an accelerating U.S. market.”

Guidance was just as impressive.

Palantir said it expects revenue to be between $1.797 billion and $1.801 billion, above the $1.68 billion estimate. For the full-year, Palantir said it expects revenue to be between $7.65 billion and $7.662B, above the consensus estimate of $7.24 billion. The company also raised its U.S. commercial revenue guidance, as it now expects sales in the segment to be more than $3.224B, up at least 120% year-over-year.

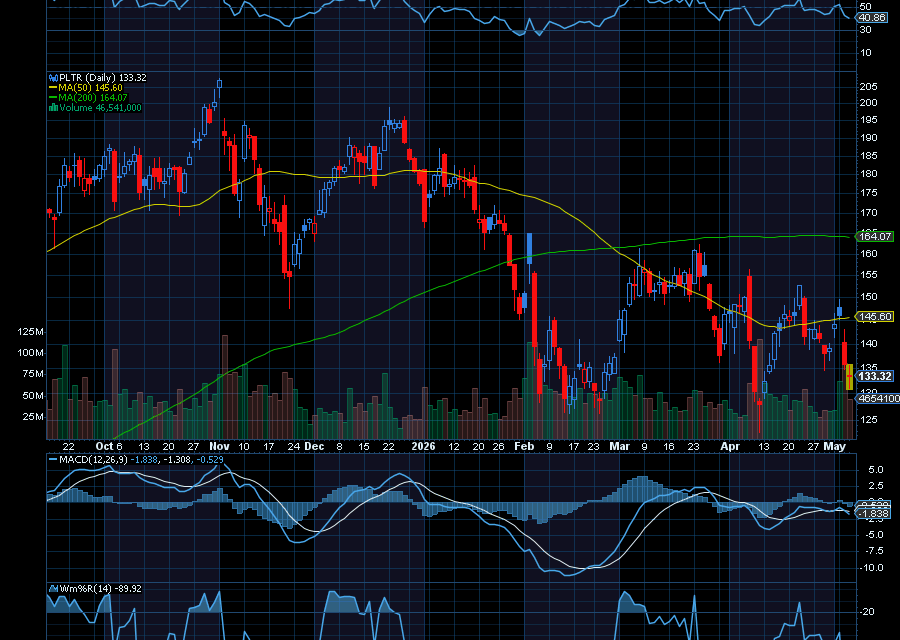

And Yet, the Palantir Stock Sank $10 a Share

Following that report, shares of Palantir slipped about $10 a share.

That’s because those results weren’t good enough for some analysts. Analysts at Jefferies, for example, were quick to point out weak spots. According to the firm, there was a slight miss in the U.S. commercial segment. It was also the first deterioration the firm had seen from Palantir in the last two years, adding that U.S. commercial sales missed expectations of $605 million.

In addition, new contracts picked up in the quarter increased by 61% year over year. But that’s slower quarter over quarter, and could be a sign of slower growth moving forward.

Also, as noted by Morgan Stanley, “the reaction suggests that ‘shares need to grow into [their] current valuation to get rewarded,’” as noted by MarketWatch.com. “Shares recently traded at about 34 times estimated sales for 2027 and about 56 times estimates for free cash flow in that period, ‘with peak growth likely approaching or having already materialized.’”

DA Davidson analysts lowered their price target on PLTR to $165 from $180, noting that the stock trades at a significant premium to peers.

Meanwhile, Wedbush’s Dan Ives said this was another “validation moment” for PLTR. Ives has an outperform rating on the stock with a $230 price target. He says demand for Palantir’s AI products is still very strong, especially from commercial customers.

Loop Capital is just as bullish.

The firm has a buy rating on the stock with a $220 price target, noting that while valuation is a concern, it’s tough to ignore the company’s strong momentum.

In short, the company is clearly firing on multiple cylinders, with accelerating demand for its AI-driven platforms and strong momentum in its core U.S. business.

At the same time, valuation concerns and even minor signs of slowing growth can be enough to shake investor confidence in the short term. For long-term investors, though, the bigger picture hasn’t changed much. If Palantir can continue to execute and capitalize on the expanding AI market, periods of volatility like this may end up looking more like noise than a warning sign.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments