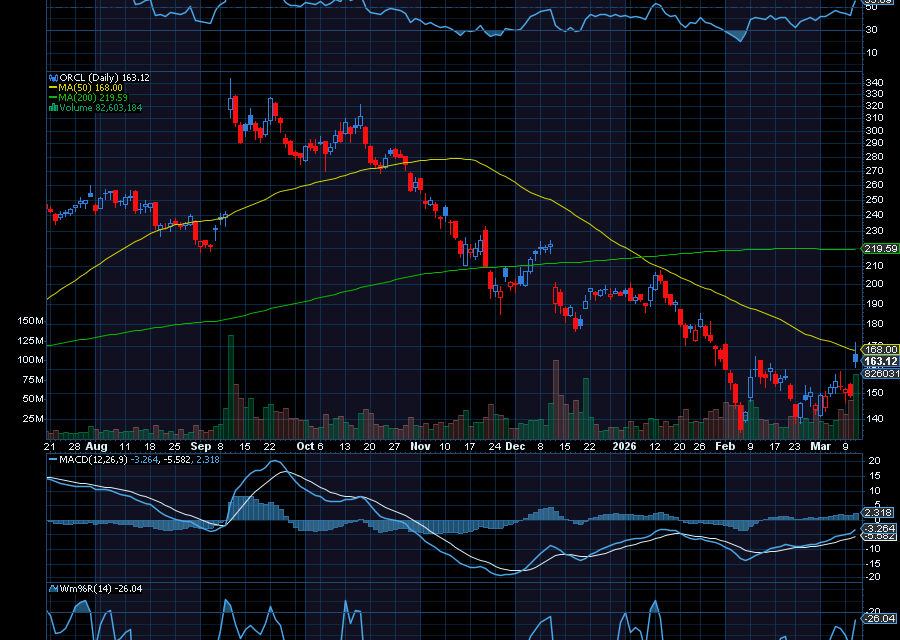

On February 25, we noted, “After seeing Oracle catch strong double bottom support at around $140, we’d like to see it retest $175 initially. Also, while we wait for ORCL to recover lost ground, we can collect its dividend. Oracle (has maintained a consistent record of dividend payments. In March 2025, the Board declared a 25% increase, raising the quarterly dividend to 50 cents per share. The most recent dividend, was paid on January 23.”

Oppenheimer analysts were bullish with a $185 price target. Analysts at DA Davidson upgraded the stock to a buy with a $180 price target.

While it’s not nearly $180 just yet, it last traded at $165 on strong earnings and guidance.

All after Oracle beat third-quarter numbers and raised guidance.

For Q3, EPS of $1.79 beat by 10 cents. Revenue of $17.19 billion, up 21.7% year over year, beat by $280 million. Cloud revenue was $8.9 billion, up 44% year over year. It was also above the estimates of $8.84 billion.

Oracle also said it expects revenue to grow between $18.93 billion and $19.24 billion. Analysts were expecting $19.11 billion. Cloud revenue is expected to grow between 46% and 50%. Adjusted earnings are expected to be between $1.92 and $1.96 per share, above the $1.93 per share estimate. Oracle added that fiscal 2027 revenue will be $90 billion.

And, according to DA Davidson analyst Gil Luria, as quoted by Seeking Alpha, “This is even better than it looks on the surface because if they can actually grow Oracle Cloud at reasonable margins, that means this is a double-digit and higher earnings growth rate company.”

In addition, analysts at JPMorgan upgraded the ORCL stock to overweight with a price target of $210 a share. RBC Capital reiterated its sector perform rating with a $160 price target. Jefferies reiterated its buy rating on Oracle with a $320 price target.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments