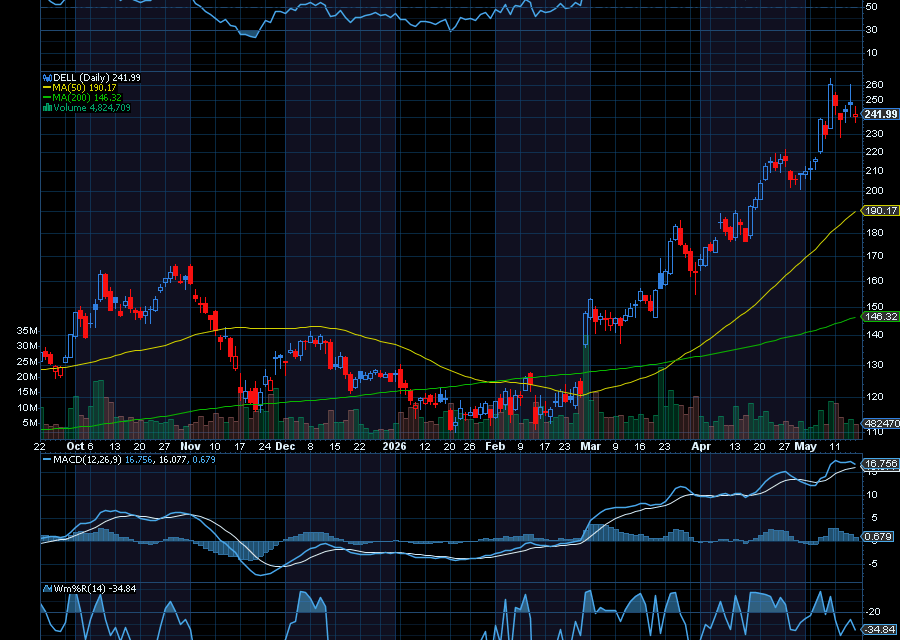

Dell (NYSE: DELL) has been one of the market’s most explosive stocks.

In fact, after bottoming near $120 in March, the tech giant has surged to roughly $248. Now, as Dell approaches its first-quarter earnings report on May 28, Wall Street analysts remain overwhelmingly bullish. JPMorgan Chase recently reiterated its Buy rating on Dell and maintained a $280 price target.

“We are expecting Dell to raise its earnings guidance for FY27 (Jan-end) again from the already raised outlook of 25% growth, although more modest in this case, on account of flow-through of the beat in F1Q27 but constrained by supply visibility which still needs to catch up to the higher demand outlook for AI servers in particular,” the firm said, according to CNBC.

Meanwhile, analysts at Citigroup raised their price target on Dell to $290 from $235, citing “strong neocloud/sovereign AI demand and improving enterprise mix” as key growth drivers, according to Seeking Alpha.

Analysts at Mizuho Financial Group also boosted their Dell price target, increasing it to $300 from $260. The firm pointed to agentic AI workloads as a durable catalyst for sustained server demand and recurring revenue growth.

What Wall Street Expects from Dell Earnings

Over the past year, Dell has transformed from a traditional PC company into one of Wall Street’s premier artificial intelligence infrastructure plays.

The company’s rally has been fueled by surging demand for AI servers powered by NVIDIA GPUs, large-scale enterprise and hyperscaler orders, and growing expectations that Dell will remain a major beneficiary of the AI spending boom.

Heading into earnings, expectations are high for big numbers.

Analysts expect Dell to report fiscal first-quarter revenue in the mid-$35 billion range, with adjusted earnings per share projected between $2.90 and $3.00. Investors will also be closely watching the company’s guidance for the remainder of the fiscal year.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments