by Tom DeMark

Options straddles and combinations are a unique way of capitalizing on market activity or market consolidation. Straddles and combinations can be utilized to make money if a trader feels the market will experience a move, but is not certain as to the direction of that move. They can also be utilized to make money if one expects the market to stabilize or consolidate over a specific period of time. Straddles and combinations are very similar. A straddle involves the simultaneous purchase of a call and a put, or the simultaneous sale of a call and a put, of the same security, strike price, and expiration date; while a combination involves simultaneous sale of a call and a put, of the same security, but with different strike prices and different expiration dates, or both different strike prices and different expiration dates. Unlike spreads, where four possible positions can be taken, there are only two sides to straddles and combinations, long and short. Here we are going to cover the long side.

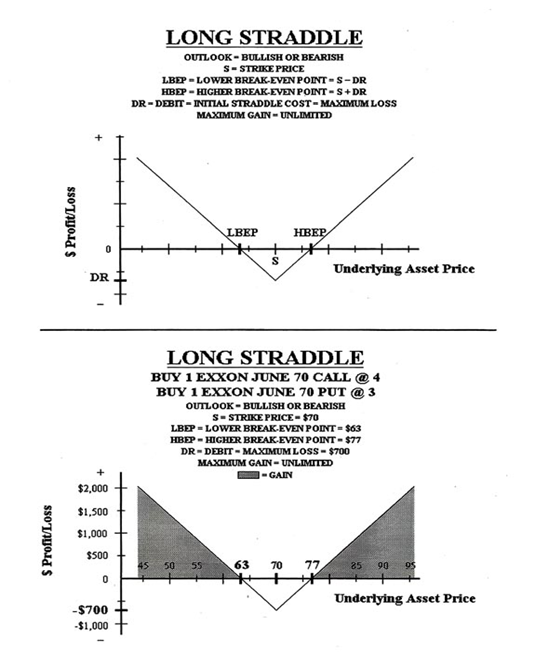

Long Straddles

In a long straddle, the trader believes the market will make a sizable move, but is uncertain of the direction of that move. This option strategy is especially common when a trader is anticipating that a news release or earnings report will have a dramatic impact on the price of an asset. A long straddle entails the simultaneous purchase of a call option and a put option of the same security, strike price, and expiration date. The long call option allows the trader to gain if it were to expire in-the-money, and the long put option allows the trader to gain if it were to expire in-the-money; if both options were to expire at-the-money, meaning the market neither advances or declines, then the trader loses what was paid in premium for both the options. Since the trader is purchasing both a call option and a put option, the trader must pay the option writers for both contracts, making this a debit straddle. So, in order to profit on the trade, one must first recoup the total cost of the straddle. To obtain the break-even points of a long straddle, one would add the net cost of the straddle to the long call option’s strike price –anything above the upper (call option’s) break-even point would be a profit and anything below the lower (put option’s) break-even point would be a profit. The maximum gain for a long straddle is unlimited, while the maximum loss for a long straddle is simply the total cost of the option premiums.

Example:

Buy 1 Exxon (XON) June 70 Call @ 4

Buy 1 Exxon (XON) June 70 Put @ 3

Market price of Exxon Stock: $70

In this example, the trader has initiated a long straddle since the security, the strike prices, and the expiration months are all the same. In this instance, one Exxon call option with a June expiration and a $70 strike price for $400 has been purchased and one Exxon put option with a June expiration and a $70 strike price for $300 has been purchased, when Exxon is trading at $70 per share. Therefore, the total cost of the straddle is $700. This is a nonrefundable, fixed cost to the trader and cannot be recovered. This $700 is also the most a trader can lose on the transaction –if both the call and the put option were to expire at-the-money, meaning Exxon stock were trading at $70 per share, the trader would lose $400 on the long June 70 call and would lose $300 on the long June 70 put. Ideally, the trader would like to see the market advance or decline dramatically. If Exxon stock were trading at $75 per share, the trader would make $500 on the long June 70 call option position that is in-the-money, make nothing on the long June 70 put option position that is out-of-the-money, and lose $700 for the fixed cost to initiate the straddle, for a net loss of $200. If Exxon were trading at $65 per share, the trader would make nothing on the long June 70 put option position that is out-of-the-money, make $500 on the long June 70 put option position that is in-the-money, and lose $700 for the fixed cost to initiate the straddle, for a net loss of $200.

Please note that a long straddle is simply made up of two regular option contracts. Therefore, as Exxon’s market price continues to move in-the-money, either upside or downside, profits continue to grow indefinitely. Long straddles differ from spreads in that the gains are not limited.

To summarize, the most the trader could lose in a long straddle would be the cost of the straddle ($700) and this would occur if the options expired at-the-money ($70). The most the trader could make in a long straddle is unlimited to the upside and restricted to the total value of the underlying contract if it were to decline to zero ($7000 – $700 = $6300) on the downside. Therefore, if the market were to advance or decline, the trader will gain; however, if the market were to move sideways, the trader will experience a loss. See the diagram below.

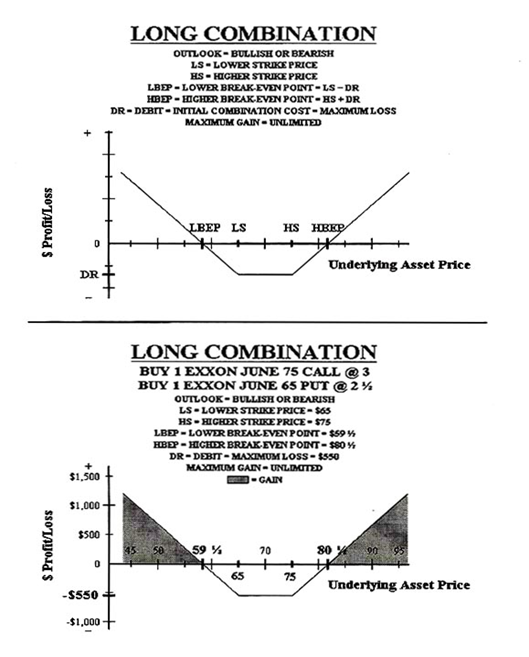

Long Combinations

A long combination is very similar to a long straddle. In a long combination, the trader believes the market will make a sizable move, but is uncertain of the direction of that move. A long combination entails the simultaneous purchase of a call option and a put option of the same security, but with different strike prices, different expiration dates, or both different strike prices and different expiration dates. (However, long combinations with differing strike prices are the most common). The long call option allows the trader to earn a profit if it were to expire in-the-money; if both options were to expire out-of-the-money, meaning the market neither advances nor declines, then the trader loses what was paid in premium for the options. Since the trader is purchasing both a call option and a put option, the trader must pay the option writers for both contracts, making this a debit combination. Consequently, in order to profit on the trade, one must first recoup the total cost of this combination. To obtain the break-even points of a long combination, one would add the net cost of the combination from the long put option’s strike price – anything above the upper (calls option’s) break-even point would be a profit and anything below the lower (put option’s) break-even point would be a profit. Any price in between these two levels would be a loss to the trader. The maximum gain for a long combination is unlimited, while the maximum loss for a long combination is simply the total cost of the option premiums.

Example:

Buy 1 Exxon (XON) June 75 Call @ 3

Buy 1 Exxon (XON) June 65 Put @ 2 ½

Market price of Exxon Stock: $70

In this example, the trader has initiated a long combination since the security and the expiration months are the same, but the strike prices are different. The advantage of this long combination is that the premiums will be lower than those for a long straddle because the strike prices are spaced further apart, creating a larger window for losses. Here, the trader has purchased one Exxon call option with a June expiration and a $75 strike price for $300 and has purchased on Exxon put option with a June expiration and a $65 strike price for $250, when Exxon is trading at $70 per share. Therefore, the total cost of the combination is $550. This is a nonrefundable, fixed cost to the trader and cannot be retrieved. This $550 is also the most the trader can lose n the transaction – if both the call and the put options were to expire at-the-money or out-of-the-money; meaning Exxon stock were trading at $65 per share, $75 per share, or somewhere in between, the trader would lose $300 on the long June 75 call and would lose $250 on the long June 65 put. Again, the trader would ideally like to see the market advance or decline dramatically. If Exxon stock were trading at $80 per share, the trader would make $500 on the long June 75 call option position that is in-the-money, make nothing on the long June 65 put option position that is out-of-the-money, and lose $550 on the fixed cost to initiate the combination, for a net loss of $50. If Exxon were trading at $60 per share, the trader would make nothing on the long June 75 call option position that is out-of-the-money, make $500 on the long June 65 put option position that is in-the-money, and lose $550 for the fixed cost to initiate the combination for a net loss of $50.

To summarize, the most the trader could lose in a long combination would be the cost of the combination ($550) and this would occur if the options expired at-the-money or out-of-the-money (greater than or equal to $65 and/or less than or equal to $75). The most the trader could make in a long combination is unlimited to the upside and restricted to the total value of the underlying contract if it were to decline to zero ($6500 – $550 = $5950) on the downside. Therefore, if the market were to advance or decline, the trader will gain; however, if the market were to move sideways, the trader will experience a loss. See the diagram below.

{kind=link}

Recent Comments