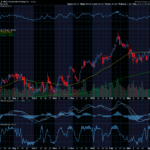

The trading action throughout last week brought us another major move higher in this incredible recovery off of the early April lows.As I said headed into the week, stocks had run into significant resistance levels, and a major catalyst was going to be required in order to push stock prices higher through those resistance bands. Last week, investors received exactly this, a major catalyst. Headed into the week, U.S. and Chinese officials met all weekend to begin talks on resolving our current trade dispute. Markets and investors’ hopes and best case scenario were that these talks would go well and a clear plan for a path forward for further talks would be the conclusion of these meetings. Well, investors got this and much more as both countries extended an olive branch to one another by temporarily pausing the ‘reciprocal’ & retaliatory tariffs for at least 90 days, dramatically lowering the current tariff level which amounted to a trade embargo. Investors had little if any hope that this would be one of the developments from these meetings but once we got the positive surprise, investors gained more enthusiasm and sent stocks soaring through the resistance levels that had previously proven tough to crack. By the week’s end the S&P 500 had rallied for five consecutive days and each of the three major averages took a substantial leap higher.

Diving into the technicals after last week’s move provides us with some very encouraging data. I had said coming into the week that 5700 on the S&P 500 as well as the index’s 200-day moving average were the clear resistance levels facing stocks. After the major trade news, both of these barriers were broken through on Monday morning! Better yet, we got clear confirmation of follow through of this move. Every day this past week the S&P 500 closed above both of these prior resistance levels which have now flipped to significant support levels underneath this market. After first experiencing a 21.3% peak to trough decline in the S&P during the first few months of the year, after the late April recovery which is still running, stocks have now bounced back by 23.2%. Also, believe it or not, after last week, the S&P 500 is now positive on the year, up 1.3% YTD! This major recovery has surprised many investors as few expected the near V-shaped recovery that we have seen thus far. Most investors with an optimistic outlook, including myself, were expecting a more W-shaped recovery with stocks ultimately resolving to the upside. But as positive trade news has been announced, stocks have begun to anticipate further good news and leaped higher in short order. Last week’s trading brought a notable breadth thrust that should not be understated. Even as the major indexes have not quite recaptured their all-time highs, the NYSE Advance Decline Index soared to make a series of new all-time highs last week. This is indicative of truly how strong the buying pressure was last week. Now looking ahead, there are not really any significant resistance levels between where the S&P 500 is trading right now and the all-time highs that were set earlier this year. There is essentially just an air pocket between here and there and while stocks will likely need further positive news to recapture those levels, it seems that this is squarely where Bulls are focused at the moment. With all of that said, after last week’s massive move higher, broadly speaking, many stocks as well as the indexes find themselves in the short term to be pretty overextended according to the technicals. The 5-day RSI for the S&P is at nearly 92 as of Friday’s close, a level that does not generally persist for long. So, I fully expect that stocks will likely take a moment to catch their breathe this week after the furious rally we have experienced over the past few weeks. Should we continue to get good news on trade policy and economic data, these could be the catalysts needed to push stocks back toward the all-time highs over the next month.

🚨 Have you heard about my WPO Newsletter, that recently gave my members the chance at a 148.9% profit opportunity? Go ahead and Click Here to begin your trial for JUST $1 Today! 🚨

Key Events to Watch For

- Trade Policy Progress

- U.S. Treasury Market (10-Year Yield)

- Remaining Q1 Earnings (HD, PANW, TJX)

On the heels of last week’s significant move higher in the market, still the primary thing that investors will be keeping their eyes on will be developments with trade policy and tariffs. Of late, we have continued to get positive headlines on this front which has provided an immense boost to the market. There is a sense out there that a handful of additional trade deals are on the precipice of being finalized. Any further deals that are completed, that include favorable terms, will add to the tailwind behind stocks. Additionally, while the U.S. and China are currently in the 90-day pause period to negotiate, further developments here will also move stocks. Investors will be hoping to see more results in the weeks to come.

Last week, even as stocks were ripping higher, traders were largely ignoring another big move that occurred in the background, the rise in U.S. Treasury yields. The specific U.S. Treasury that I am focusing on is the 10-Year U.S. Treasury. Less than one month ago, in early April, just as peak panic was hitting markets, treasury yields went flying higher as investors feared that foreign investors were losing interest in, if not outright dumping U.S. government debt in response to the trade war. This was an unusual move given the circumstances, because generally investors will pile into U.S. Treasuries in moments of high fear and volatility, thus driving the yields lower, however, in that moment, the exact opposite occurred. This drove the yield on the 10-year higher in rapid fashion, rising 70 basis points in six trading days, a move that has little precedent in such short fashion. During that move, the yield topped out between 4.5%-4.6%, which further spooked investors as this raises borrowing costs for businesses and consumers. Well, last week, while stocks were rallying day after day, the yield on the 10-year creeped right back up to this range, trading above 4.5% on several occasions. Now arguably, the 10-year yield has risen this time for good reasons as recent economic data has come in better than most had feared, while previously, yields were backing up for quite negative reasons. Regardless, the 10-year yield has risen back to this range where investors balked previously and this will continue to squeeze businesses and consumers when looking for credit. Furthermore, on Friday after the close, major ratings agency Moody’s revealed that they finally joined their two colleagues, Fitch & Standard & Poor’s, in downgrading the U.S. government’s credit rating by one notch from AAA, down to AA+. All three ratings agencies made this decision over the past few years due to concerns about the size of the U.S. government’s debt & the size of deficits that we are currently running. While how much of an effect this will have on yield levels is a debate to be had, having the U.S. government’s creditworthiness downgraded yet again will almost certainly provide further upside pressure on the yields that bond investors will demand when buying U.S. government debt. This week it will be important to watch out for any early effects due to this credit downgrade.

There are not too many more noteworthy Q1 earnings reports to go as this reporting season has largely come and gone now that more than 90% of S&P 500 companies have already posted results. With that said, there are a few reports this week that our team will be keyed in on. On Tuesday, there are two reports we’ll be watching for as Home Depot, Inc. (HD), & Palo Alto Networks, Inc. (PANW) both report. HD will report in the premarket hours, while PANW will report once the market closes. In addition to these reports, the following day, on Wednesday, TJX Companies, Inc. (TJX) will report their earnings before the market open. In addition to a clear update on each company’s business health, each of these reports will provide a helpful lens into different parts of the economy.

Thank you for reading this week’s edition of the Weekly Market Periscope Newsletter, I hope you enjoyed it. Please lookout out for the next edition of the newsletter as we will give you a preview of the upcoming week’s important market events.

Thanks,

Blane Markham

Author, Weekly Market Periscope

Hughes Optioneering Team

{kind=link}

Recent Comments