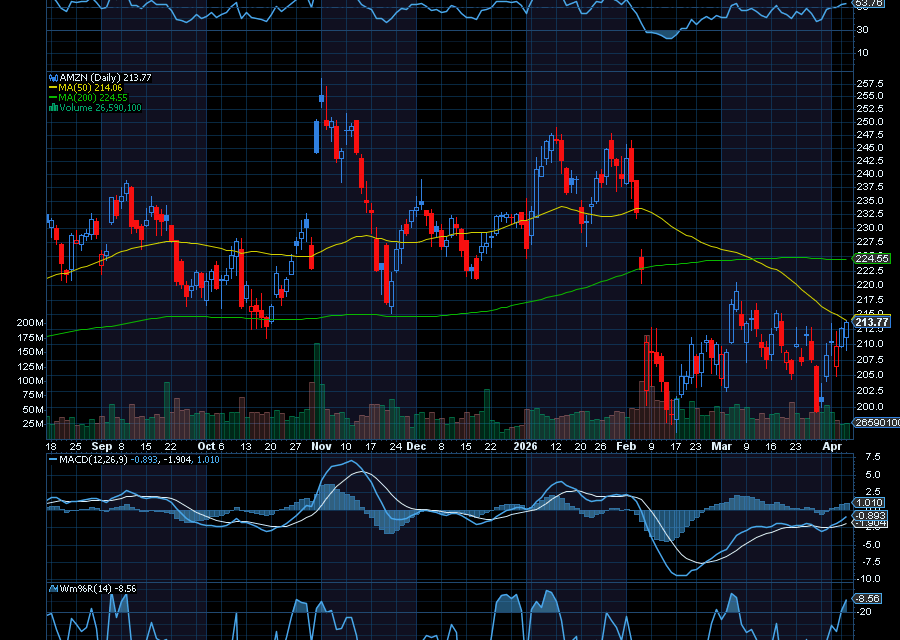

Keep an eye on Amazon (AMZN).

Amazon is trading at less than 28x forward earnings — historically low compared to its 10-year average. This discount comes at a time when the company’s growth catalysts remain strong. AWS, Amazon’s cloud segment, is benefiting from the growing demand for AI infrastructure.

Also, while the market has reacted negatively to short-term headwinds such as increased capital expenditures, margin pressure, and intensified competition, these concerns appear overblown. In addition, analysts at BNP Paribas, for instance, say investor worries about AI-related spending are overdone.At the moment, the firm has a $320 price target on Amazon, signaling significant upside potential. Overall, the combination of undervaluation, strong growth catalysts, and the AI boom makes Amazon an attractive opportunity.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments