by Don Wellenreiter

There are a few things you should know about options & futures contract specifications. Futures contracts (but not options) have letter designations that tell you what the month of delivery is, and your broker may use them or ask you to use them.

They are as follows:

January = F

February = G

March = H

April = J

May = K

June = M

July = N

August = Q

September = U

October = V

November = X

December = Z

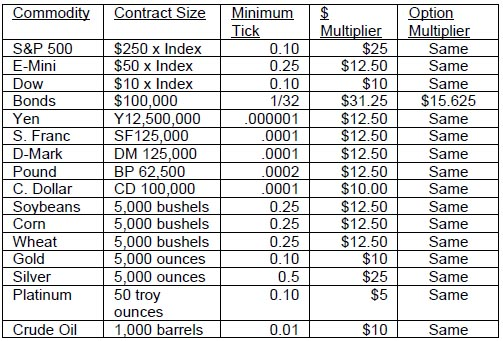

Option strike prices DO NOT have their own letter or symbol in the commodities business. But they do in equities trading, where all contract sizes and dollar values are constant. As you will see in the chart below, commodity contracts are all very different from one another.

One of the more confusing aspects to commodity trading is that they all have different values. This is particularly true with the bond contract and its option, both of which have different tick and dollar values. Below you will find just a few of the more widely traded contract specifications. You should always ask your broker for the current margin requirements for a given commodity, as well as a given trade, since the margin requirements change with market conditions. All quotes below are the courtesy of CQG, Inc, a commodity and stock quote vendor.

As you may have noticed, the Treasury bond offers a twist in its calculation of its option price. For the beginning trader, this market can be truly confusing. Let us first start with the bond future. Bonds are traded in thirty-seconds, so 32/32 equals one-full point in this market. If it were 64/32 it would be two points. Let’s say the current daily limit move in bonds is 96/32 or three full points. One full point equals $1,000. This is derived by taking 32 x $31.25 (its point value from above) to equal $1,000. One-half point move, or 16/32 would equal $500 (16 x $31.25).

Now it gets weird. Bond options are one-half that of the futures contract. They trade in sixty-fourths, while each “tick” or minimal movement equals $15.625 ($31.25 divided by 2 = $15.625). A full point move in the bond option is 64/64ths, where a half point move is 32/64ths.

To make matters worse 64/64 is also referred to as 100. An option trading at 107 is not 107 x $15.625 = $1,562.50. It is broken down to 64 x $15.625 = $1,000 plus 7 x $15.625 = $109.375. The total would then be 1,109.375. You may also simply add the 7 ticks in this example to the 64 to get 71 ticks. Then it would be 71 x $15.625 = $1,109.375.

Review this several times because it can be very confusing. If it is too much for you, simply trade any of the other dozens of markets available to you. You can also review this with your broker for further explanation.

To give you an idea of the immense leverage that exists in commodities trading, one contract of a Treasury bond can have a margin of roughly $2,500 (all margins are subject to change without warning). That $2,500 margin deposit now controls a contract with a face value of $100,000! So for about 2.5% you can control a position worth 40 times the money you put up!

This can be good or bad; ask any bond trader. If the same current rules applied in this market as they do in the stock market where margins are generally 50% across the board you would need to put up $50,000 to hold this very same bond contract.

This means that a 2.5% move in the Treasury bond contract could earn you a 100% return on your margin deposit – or lose you 100% of your margin requirement, depending on what side of the market move you are on. Remember that you can always lose more than your original margin deposit when trading futures, sometimes significantly more!

{kind=link}

Recent Comments