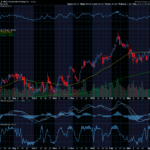

We finally saw stocks defy the status quo from the previous two weeks as we did not have momentum sputter in Friday’s trading session. Instead, several major averages finished the week closing at all-time highs! In quite an impressive recovery, the S&P 500 has completed its V-shaped roundtrip from the February highs to the April lows, now back to all-time highs! For the patient and long-term focused market Bulls, these new highs have been long awaited since the early April lows. For several weeks prior to last week, the S&P 500 had been tightly rangebound with a lid over stock around roughly 6050. This level of resistance held firm until last week when one major point of uncertainty was seemingly resolved. Towards the finale of Monday’s trading session, the market clearly began to sniff out that the war with Iran was in its closing frames and was nearing an end. By the end of the day, stocks had rallied to near session highs and the market had made its bet. Shortly after U.S. markets closed it was announced that a ceasefire agreement had been reached between all involved parties in the war and this development was greatly cheered by equity investors! Quickly thereafter, the price of oil collapsed, along with it the inflation-hawks fears about rising energy prices. This was exactly the type of catalyst that we have been waiting for to propel stocks back to fresh highs. As this significant geopolitical uncertainty cleared, the path to new highs was wide open. As the week progressed, several Fed members expressed openness to the idea of a rate cut at the upcoming July meeting. This included Fed Chair Powell as he signaled that it is possible that the pass-through effects of tariffs could perhaps not be as great as feared, which would allow the Fed more leeway to consider rate cuts sooner. Then finally, one additional piece of good news provided the last thrust needed to boost stocks to new highs. Thursday’s initial jobless claims came in a bit lighter than expected, which was a huge relief (at least in the short term) for investors. Concerns about rising initial claims had cropped up lately but seeing this number come in cooler than expected was music to the ears of investors. Having massaged away these areas of concern throughout the week kicked off a wave of bullish optimism. This combination of positive headlines was enough to push the Nasdaq to new highs on Thursday and then again alongside the S&P 500 index on Friday!

Now that several of the major indexes are yet again trading at all-time highs, I think it’s a good idea to look under the hood at the market internals & the technicals to see what kind of staying power this rally really has. In just the past week we have seen some improvement in the breadth of this rally. Prior to last week, less than 50% of S&P 500 stocks were trading above their 200-day moving average. As of Friday’s close, now 51% are above this mark, which is a nice sign that the rally could be broadening out. While we are still looking to gain steam over the longer-term, if we zoom in just a bit, stocks are broadly showing a great deal of upside momentum in the intermediate term. At the close on Friday, nearly 71% of S&P 500 stocks were trading above their 50-day moving average. This is a signal that broadly stocks are building constructive trends. So far, the trends are only medium term breakouts but soon many of these could become longer term breakouts which would be an additional positive for investors. Furthermore, last week we also saw the S&P 500 Advance/Decline line break out to a new all-time high. This is an additional sign of broadening strength in the markets. The technicals for the actual S&P 500 index itself are quite impressive as well. The index has now broken through resistance at the old highs and is still making a strong series of higher highs and higher lows. Also, I need to add that the “Golden-Cross” Buy signal on the S&P 500 is almost assuredly set to trigger this week, most likely on Tuesday or Wednesday. This will be a hugely important technical buy signal for the market, so watch out when this happens. Historically this precedes a strong rally to come in the subsequent 10-12 months. With all of that said, following last week’s major thrust higher, at the index level, stocks have found themselves squarely in short-term overbought territory according to several metrics. In this shortened week of trading ahead, don’t be surprised to see the indexes retreat somewhat to allow investors the chance to digest the recent move and consolidate gains before ultimately continuing to trade higher from there.

⚡ Special Promo: First Month Access for Only 1$⚡

Have you joined my Weekly Profit Opportunity newsletter yet? If not, then you just missed out on a recent trade alert I sent to members that has risen 62.5% in just a few weeks! While past results do not guarantee future returns, this newsletter features my top trade pick each week!

Key Events to Watch For

- U.S. Trade Policy (Pending Trade Deadline)

- Budget/Tax Cut Bill Progress

- Jobs Report – June ‘25

After a week when investors finally witnessed stocks break out to new all-time highs once again, it’s important to look forward and anticipate which factors will drive stocks from here. It seems clear now, as more pressing geopolitical matters have cooled, the market is squarely focused back on U.S. trade policy and any developments as they break. Upcoming on July 9th, is the self-imposed deadline when the reciprocal tariff ’90-Day pause’ is set to expire. Admittedly, President Trump has said that not too much attention should be paid to this date, presumably because the ‘pause’ could just be extended further. Still, until this is made clear, it would be wise to take note of this date. The end of last week brought a mixed bag on trade policy news. On one hand, investors got a positive as further progress in trade negotiations with China was announced. However, later in the day on Friday, a story broke that the U.S. was ceasing all trade negotiations with Canada and would soon be announcing the “final” tariff rates assigned to that country. So just as investors saw new highs on the market, tariff fights and negative trade policy headlines returned front and center. If we get back into a game of tariff policy ‘whack-a-mole’, like we saw earlier this year, this could put some short-term pressure on stocks. Investors will be hoping for quick resolution to a few of these trade policy overhangs.

Speaking of upcoming, self-imposed deadlines, there is another one on our radar too. The July 4th deadline to pass the current budget/ tax cut bill, dubbed the “Big, Beautiful Bill”, is coming up fast. Now, certainly there is not a hard cut off here, but it’s been well telegraphed that the administration wants this bill passed by this date. The bill has drawn significant attention from Wall St. for several reasons. Primarily, the main focus of the bill is to extend the current TCJA tax cuts which are set to expire at the end of the year, which would have a stimulative effect. However, there is another side to this debate as well. Many projections estimate that despite any stimulative effects from the bill, as it exists now would result in a further expansion of the U.S. fiscal deficit. In a context when bloated U.S. deficits are a lingering concern for investors, any news around this bill could move markets. Currently markets are all but pricing in that the bill will pass and the tax cuts will be extended. However, should some uncertainty present itself here, for example, the bill being delayed or having to be re-worked significantly, this could upset stocks in the short term as it would defy the baked in assumption.

This coming week will feature several new pieces of macroeconomic data, but there is one principal data point that I am focusing on. This would be the Jobs Report from June. The current estimates are that in June we will have seen a bit further slowing in the job market nationwide as non-farm payrolls are projected to still grow but at a slower pace and also unemployment is expected to tick up to 4.3% from 4.2% last month. This would corroborate other recent data which seems to indicate that the labor market is softening. While still far from cracking, a growing pool of evidence suggests the jobs market is getting tighter, and this could put pressure on the Fed to push up their timeline for their two projected rate cuts this year.

Thank you for reading this week’s edition of the Weekly Market Periscope Newsletter, I hope you enjoyed it. Please lookout out for the next edition of the newsletter as we will give you a preview of the upcoming week’s important market events.

This market is fast and furious and getting insight as it happens is key to trading success. To give you live market insight we are launching Trade of the Day LIVE. Click here to sign up for the next live room and make sure you are there.

Thanks,

Blane Markham

Author, Weekly Market Periscope

Hughes Optioneering Team

{kind=link}

Recent Comments