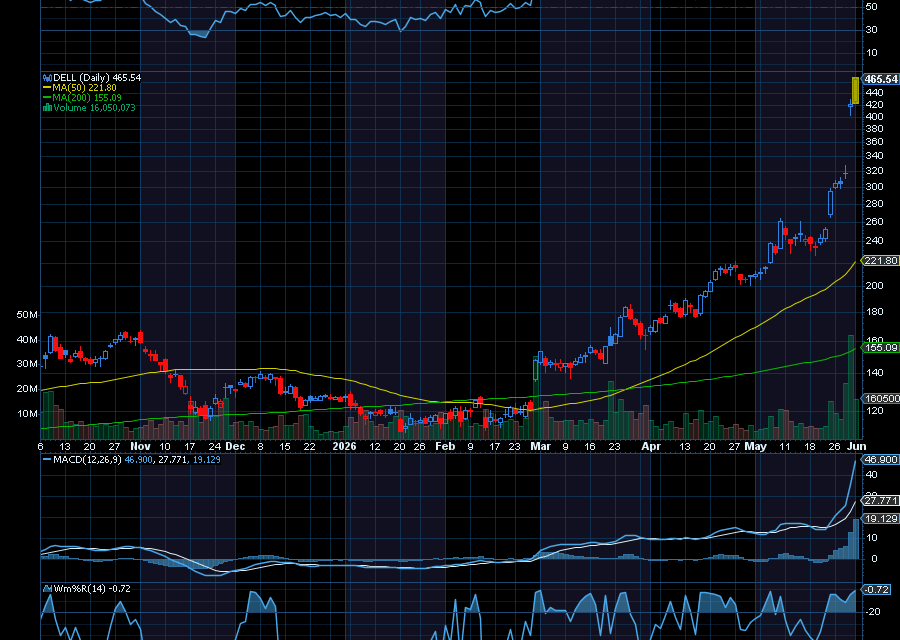

Just the other day, we highlighted an opportunity in Dell (NYSE: DELL), which exploded late last week. Once known primarily as a PC manufacturer, the company has emerged as one of the biggest beneficiaries of the artificial intelligence boom, thanks to surging demand for its AI infrastructure and server business.

Investors have flocked to the stock as demand for AI servers powered by NVIDIA GPUs continues to accelerate, driven by enterprises and hyperscale cloud providers racing to expand their AI capabilities. While the stock may be due for a short-term pullback after its impressive run, Dell’s long-term growth story appears firmly intact.

Blowout Quarterly Results

The company’s latest earnings report highlights just how strong that momentum has become.

In the first quarter, Dell reported earnings per share of $4.86, crushing Wall Street expectations by $1.96. Revenue surged 87.5% year over year to $43.8 billion, exceeding analyst forecasts by $8.46 billion.

Much of that growth came from the company’s booming AI business. Dell booked $24.4 billion in AI orders during the quarter and generated $16.1 billion in AI server revenue.

“Our record Q1 performance reflects strong in-quarter demand, as well as our pace of innovation across the full stack of PCs, compute and storage,” said Vice Chairman and Chief Operating Officer Jeff Clarke.

AI Demand Shows No Signs of Slowing

Management’s outlook suggests the growth isn’t slowing anytime soon. Dell raised its fiscal 2027 AI server revenue forecast to $60 billion, underscoring its confidence in continued AI spending across the industry.

The company expects second-quarter revenue between $44 billion and $45 billion, with non-GAAP earnings per share of approximately $4.80. For the full fiscal year, Dell projects revenue of $165 billion to $169 billion and GAAP earnings per share of $17.90, reflecting management’s confidence in both AI demand and broader business performance.

Wall Street Turns More Bullish

Investors weren’t the only ones impressed by the results. Several major Wall Street firms raised their price targets following the earnings release.

Susquehanna upgraded Dell to Positive from Neutral and dramatically increased its price target to $700 from $138.

J.P. Morgan maintained its Overweight rating while boosting its target to $500 from $280, citing stronger-than-expected demand and improved visibility into future revenue growth.

Even the Skeptics Are Taking Notice

The most notable was the reaction from Morgan Stanley, which currently maintains an Underweight rating on the stock.

The firm’s analysts acknowledged that they underestimated Dell’s growth trajectory, describing the quarter as one of the most impressive they have seen in the hardware sector. They pointed to several standout metrics, including nearly 100% growth in traditional servers, the fastest storage growth in 12 quarters, near-record operating margins in the PC business, and a substantial increase in full-year guidance.

The analysts noted that Dell is benefiting not only from strong market demand but also from market-share gains and strong execution across its business segments.

Citi Sees More Upside Ahead

Citi also raised its price target on Dell, increasing it to $475 from $290 while maintaining its Buy rating. According to the firm, revenue growth significantly exceeded expectations, earnings benefited from stronger margins and scale, and demand continues to outpace supply.

That supply-demand imbalance is helping support a healthy backlog that could provide visibility and growth opportunities through the remainder of the year.

In short, Dell is no longer just a PC company.

It has become a major player in AI infrastructure, and its ability to capitalize on one of the biggest technology investment cycles in decades is driving record growth. Dell’s expanding AI business, strong financial performance, and growing support from Wall Street suggest the company remains well-positioned for continued long-term growth.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments