Last week’s trading week finally brought investors a taste of exactly what they have been hoping for, progress on trade policy. On Thursday, the U.S. finally signed a new trade deal with one of our trading partners, hopefully a sign of more deals to come. The new deal was signed with the United Kingdom, a long-time top ally of the U.S. While this is certainly not among the most crucial deals that need to be done, finally having a tangible deal done is a positive sign of progress for investors. Markets had a positive reaction to this development as they rallied to a new 1-Month high before encountering resistance. The S&P 500 found firm resistance at 5700, a key resistance level which formed in mid-March and is still intact. Headed into the week it was largely expected that stocks would likely take a breather after the S&P 500 had just rallied for nine consecutive trading sessions. Despite the new trade deal along with other positive developments on the trade policy front, seeing the three major indexes finish mildly in the red for the week should come as no great surprise. This past week’s positive developments set the table for a key meeting between U.S & Chinese officials taking place this weekend. I’ll have more to say on this shortly. Bottom line, even though the averages finished slightly down this past week, finally seeing some concrete progress on the trade front is positive for the market and should we see this become a trend in weeks to come, this will provide further support for stocks.

While trade policy is sucking up all the air in the room right now and continued to dominate headlines last week, there were a number of other significant events as well. We had a Fed meeting, and the policy result was as expected, the FOMC opted to keep rates unchanged. The most important tidbit came from Fed Chair Powell’s presser in which he described continued uncertainty when trying to forecast economic conditions for the rest of the year. He stressed that at this moment, the Fed sees risks to growth, inflation, and employment to be legitimate, yet, roughly in balance which portends a tricky puzzle for the Fed. This was a delicate way to communicate that they expect at least a brief period of stagflation ahead for the American economy. Because of this, the committee seemingly plans to keep rates at current levels until there is more clarity, or macroeconomic data begins to show the risks in one of these areas to be greater than the others. Additionally, there was another major policy development from this past week that is a win for stocks. The Trump Admin, after previously signaling that they were going to further tighten export restrictions on certain A.I. related hardware, including high-powered GPUs designed by Nvidia, last week they pivoted on this. The admin reversed course after wide criticism from the Tech sector and now they seemingly will be relaxing if not totally scrapping many remaining Biden-era restrictions. This provided a nice boost for the A.I. related stocks in particular.

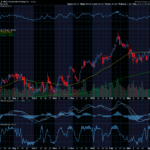

Following this last week’s action, I want to paint a clear picture of where markets currently stand. As of Friday’s close, the S&P 500 is now 17.1% higher from the early April lows. Also, we are still about 8% below the recent market high, but on the year the S&P is only down 3.7% YTD. Additionally, the volatility that we have seen in recent months has largely subsided at least for now. The VIX, while still slightly elevated, has collapsed from 60, to now below 22. Furthermore, the average true range (ATR) of the S&P 500 has also cratered, signaling the slowdown in wild intra-day price swings. As the volatile whipsawing has relaxed, this has been positive for investors. This past week’s trading continued to add to the recent constructive developments as the S&P 500 continued making new short-term higher highs and higher lows. The index also remained above its 50-day moving average for the entire week, a nice sign of technical follow through. With all of this said, it seems clear that a well-defined technical trading range is developing for the S&P 500 between roughly 5700 on the high end and 5500 on the low end. I expect in weeks to come that at the index level, this trading range will become even more apparent, and we’ll likely consolidate and trade within this range as investors await a major trade deal with significant partners. There is also clear resistance above the S&P 500 in the form of the 200-day moving average. Between this and the upper end of our recent trading range, there are some clear technical hurdles in front of stocks, however, any closes above these levels should be interpreted as a strong bullish sign.

💥Over the past year, my Weekly Profit Opportunity newsletter has given members the opportunity to profit from 94% of the trade alerts that were featured. Don’t miss your chance to try it out for JUST $1. 💥

Key Events to Watch For

- Trade Meeting with China (Other trade developments)

- Retail Sales & Inflation Reports (CPI & PPI)

- More Q1 Earnings (WMT, CSCO, AMAT)

As has been the case for weeks, our trade policy and any developments remain top of mind for most investors. While much of the shocking intra-day volatile swings seemingly have subsided, this is still the main driver behind stocks in this environment. As mentioned earlier, investors got a small reward this past week in the form of the trade deal with the U.K., but there are much bigger deals with more crucial trading partners that need to be worked out. This weekend a meeting is taking place in Switzerland between U.S. and Chinese officials where they will begin discussing trade policy between the two nations moving forward as there is a de facto embargo in place now. It would be a long shot to expect a finalized deal to come out of this meeting and markets are not expecting one. Markets need to see is one thing, de-escalation. As long as this meeting concludes with positive developments and avoids ramping up any hawkish rhetoric, the markets will take this as a step in the right direction. Prior to the meeting, President Trump even hinted at lowering current tariff levels on China from their enormously high level of 145%, down to 80%. While both are problematically high and 80% is substantially higher than what we had before this current trade war, seeing the tariffs actually move down would be welcomed by stock investors. Markets will be hoping for an outcome where this meeting goes well and for a clear plan for further trade discussions. Additionally, other than China, there are many other significant trade deals lingering that need to be worked on as well. Should we see progress on any of these fronts this will be supportive for markets too.

While investors hope for further positive news on the trade policy front, there are a handful of economic reports due this week that investors should expect will move markets. Two of these are the CPI and PPI inflation reports from April. Of these two, CPI will be released first on Tuesday, followed by PPI on Thursday. According to projections, CPI is forecasted to decline from 2.4% to 2.3%, while PPI is forecast to rise from 2.7% to 3.1%. So, a bit of a mixed picture is expected from these inflation reports. The other key economic report I’ll be watching this week will be the April U.S. Retail Sales report. This report measures what consumers actually did with their wallets in the month of April even as soft data points were collapsing. Retail sales are expected to show a modest increase of 0.1% MoM, building on the previous month’s advance. Each of these reports are crucial because they are hard tangible data points about what is actually happening out there in the economy and help to cut through the ‘noisy’ soft data that more just expresses people’s sentiment.

We are just about ready to put a bow on Q1 earnings season as 90% of S&P 500 companies have now reported their earnings. Q1 earnings have turned out to be quite a strong reporting season despite the uncertain environment we have been in. As of now, 78% of S&P 500 companies have reported EPS beats, which is higher than the long-term average. With that said, there are still a few notable companies still to report and we will hear from a few of them this week. The biggest earnings report that I’m watching this week will be from WMT who is set to report in the pre-market on Thursday. In addition to this one, I am also watching CSCO and AMAT which will report on Wednesday and Thursday respectively.

Thank you for reading this week’s edition of the Weekly Market Periscope Newsletter, I hope you enjoyed it. Please lookout out for the next edition of the newsletter as we will give you a preview of the upcoming week’s important market events.

Thanks,

Blane Markham

Author, Weekly Market Periscope

Hughes Optioneering Team

{kind=link}

Recent Comments