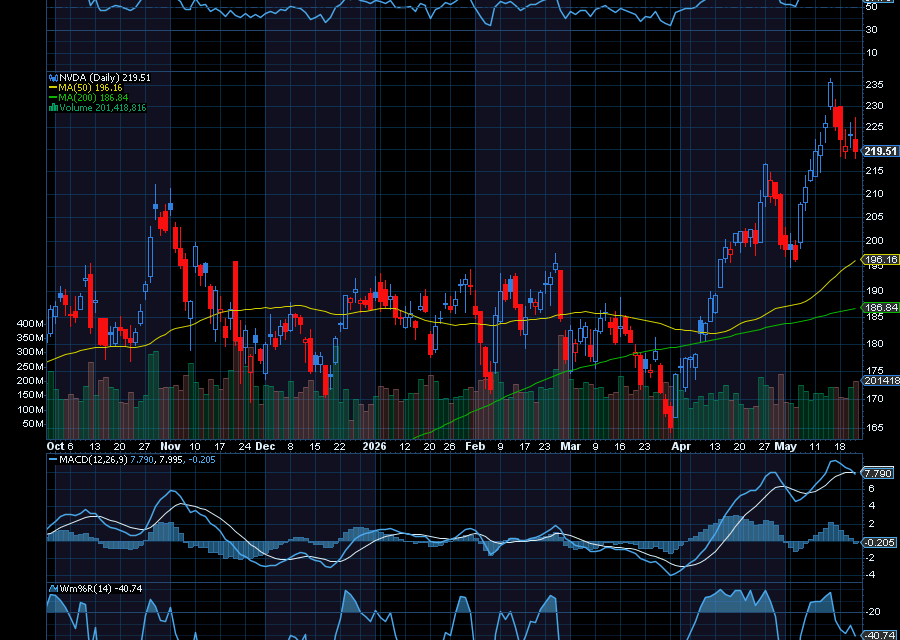

As expected, (NASDAQ: NVDA) crushed earnings, further cementing its dominance in the booming artificial intelligence (AI) market and strengthening the bullish outlook for AI stocks.

In fact, the company saw adjusted EPS of $1.87, as revenue exploded 85% year over year to $81.61 billion. Analysts had expected the company to earn an adjusted $1.75 per share on $79.19B in revenue. Moving forward, Nvidia expects revenue to be $91 billion, plus or minus 2%. The company also said that it does not expect any revenue from China for the period. Analysts had expected the company to generate $87.3 billion in revenue.

Even more impressive, Nvidia also added $80 billion to its share buyback program. And it raised its quarterly dividend to $0.25 per share, up from a prior $0.01 per share, which is payable to shareholders of record on June 4 on June 26.

And yet, that just wasn’t good enough for Wall Street.

Analysts say investors “have got used to Nvidia delivering stellar results and amid some concerns that it will face growing competition,” as noted by the BBC. “Nvidia represents 8% of the S&P 500. Unless there’s a belief in this continued parabolic growth it’s difficult for investors to get super excited, although Nvidia posted outstanding numbers.”

Another key concern is China.

During the earnings call, the company said that, “While the U.S. government has approved licenses for H200 to be shipped to China-based customers, we have yet to generate any revenue, and we are uncertain whether any imports will be allowed into the country. As a result, consistent with last quarter, we are not including any China data center compute revenue in our outlook.”

In addition, despite crushing estimates and delivering strong growth, Nvidia’s high expectations are becoming harder to justify as investors grow more cautious. Not helping, investors are concerned that Nvidia may not be able to maintain its extremely fast revenue growth forever. After several quarters of huge gains driven by AI demand, some investors fear growth could start slowing as comparisons become tougher and the market matures.

Plus, as noted by CEO Jensen Huang, the company has “largely conceded” China’s AI chip market to Huawei. “The demand in China is quite large,” Huang told CNBC. “Huawei is very, very strong. They had a record year, they’ll likely, very likely, have an extraordinary year coming up, and their local ecosystem of chip companies are doing quite well, because we’ve evacuated that market. “We’ve really largely conceded that market to them.”

Once the negatives have been priced in, we’d look to buy dips.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments