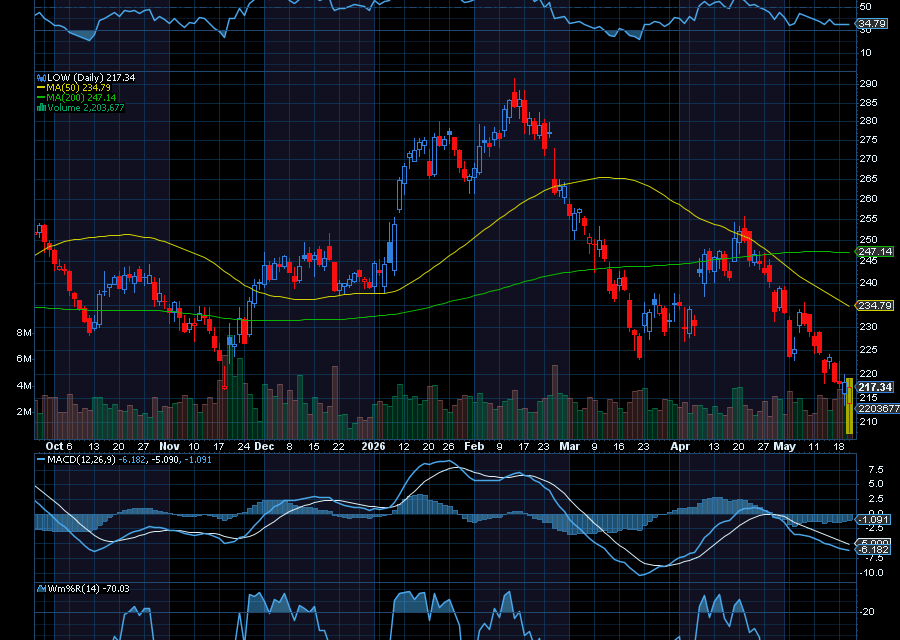

Lowe’s just reported EPS of $3.03, which beat by six cents. Revenue of $23.1 billion, up 10.4%

year over year, beat by $220 million. Comparable sales also climbed 0.6%, showing that demand for home improvement projects remains resilient despite ongoing pressure from high interest rates and cautious consumer spending.

However, even with those impressive numbers, the LOW stock slipped.

While disappointing, don’t write the stock off just yet.

The reason comes down to guidance. Lowe’s now expects adjusted diluted EPS for the year to range from $12.25 to $12.75. While that may still look healthy on the surface, the midpoint of the range falls slightly below Wall Street’s consensus estimate of $12.59. Investors were hoping for a more optimistic outlook, particularly after the company delivered a quarterly beat on both earnings and revenue.

Still, investors should not rush to write off Lowe’s just yet. For one, the recent selloff has pushed the stock into technically oversold territory. Momentum indicators such as the Relative Strength Index (RSI), MACD, and Williams’ %R all suggest the shares may have fallen too far.

In addition, analysts bullish on home improvement sector.

Citi, for example, just upgraded Lowe’s to a buy rating following the latest pullback, arguing that the worst may already be priced into the stock.

According to Citi analysts, the housing and home improvement market could see gradual improvement throughout 2026. While growth may remain modest, there is still significant pent-up demand for home improvement spending after years of elevated mortgage rates and reduced housing turnover.

“We see 2026 as a year of gradual improvement, even if the growth is slightly lower. There is pent-up demand for home improvement spending on a multi-year basis as existing home sales step up to higher levels and lower rates drive increased engagement with projects,” said the firm, as quoted by Seeking Alpha.

Sincerely,

Ian Cooper

{kind=link}

Recent Comments