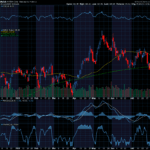

Are the VIX and other indicators indicating a short-term top to the market?

We’ve had quite a run up after inflation numbers seem to be showing that the FOMC doesn’t have to be as aggressive in the future, but perhaps the markets have gone too far too fast. The day before that, the market seemed to be prepared for a crash over a cryptocurrency problem with FTX, but the market quickly shrugged that off. The simplest indication of this general lack of concern could be from the VIX index, which is the market’s expectation of future movement in the S&P 500:

While the VIX is near 6-month lows, we see that over the last 2 trading days, the VIX is rising in spite of a rising stock market. This is an indication that traders are buying options – and that could be coming in many forms, from put buyers to hedge long stock positions, to put buyers speculating a fall, or call buyers replacing stock positions, or a number of other strategies to take advantage of rapid market movement. Traditionally, when I see the VIX rising along with stocks, I tend to think that the market participants are telling me that they aren’t full comfortable buying the market, and that’s concerning.

Perhaps one of the most logical reasons behind this buying of options is to simply look at the relative movement over the last 20 trading days and the implied volatility in the S&P 500:

*From CBOE LiveVol

As you can see, realized volatility has been significantly higher at nearly 29%, meaning that on a close-to-close basis, the market is more volatile right now than what traders expect in the future, and that’s factoring in the recent rise in the VIX. That could be a concern as those selling options right now are not being paid a premium to do so.

Additionally, one could compare the Average True Range (ATR) of the S&P 500, which illustrates the average daily range (as opposed to the realized volatility calculation, which is based on close-to-close price movement). For the S&P 500, that’s been $8.55 over the last 20 trading days. That’s about 2.15%. If one could capture that daily movement optimally by buying the low and selling the high, the realized volatility annualized would be over 34% vs a VIX of just over 24%. Again, the market is moving more than the options are pricing in.

It’s not practical to think that any trader will buy the low and sell the high every day, but it does help explain why the VIX is getting a bit of a bid here. The market is showing large ranges, and even on a close-to-close basis, the VIX looks underpriced.

There are a number of technical indicators to review in the market, as well. But I’ll save that discussion for my webinar this afternoon. Don’t forget to sign up and join me as I will be discussing the VIX, ATR, multiple technical indicators, and of course, how I look to apply this type of setup to my options trades!

So please go to http://optionhotline.com to review how I traditionally apply technical signals and probability analysis to my options trades. As always, if you have any questions, never hesitate to reach out.

Keith Harwood

Keith@optionhotline.com

{kind=link}

Recent Comments