Another week, another loss, with this one being much bigger than the previous one. All of the indices have now broken below key technical floors, and some of them are on the verge of falling under some more. The best thing going for stocks right now? The stumble was so big that it sets the stage for a dead-cat bounce that may end up getting some traction.

We’ll take a detailed look at what’s likely to be next for the market after last week’s drubbing. First, though, let’s look at last week’s major economic announcements and preview what’s coming this week. There’s not much in the lineup that’s apt to alter the market’s direction, but that’s not necessarily good thing given the direction things are moving.

Economic Data Analysis

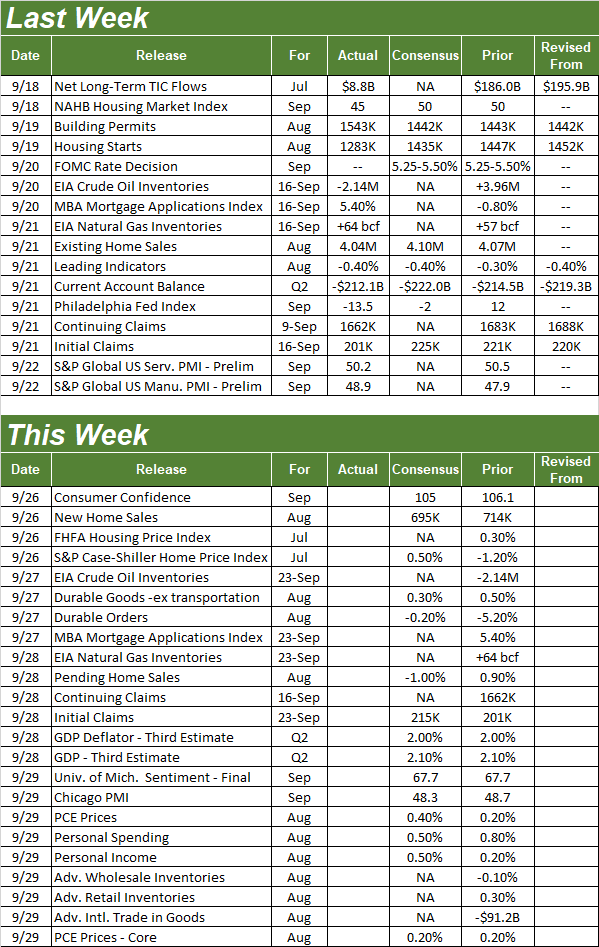

Last week’s big news was the Federal Reserve’s decision on interest rates; the FOMC left them unchanged, but one more rate hike this year is probable. But, that wasn’t the only news worth noting. It was also a big week for real estate numbers.

The party started on Tuesday, with last month’s housing starts and building permits. The former was down, and well below expectations. The latter was well up, and better than expectations. In both cases, last month’s data appears to be extending confusingly-opposing trends.

Housing Starts and Building Permits Charts

Source: Census Bureau, TradeStation

Sales of existing homes took another tumble, nearing the two-year low reached late last year. This is a concern. While prices are holding up reasonably well (more on that in a moment), this is where the weakness is showing. Part of the headwind is a lack of inventory – sales of existing homes make up the vast majority of all real estate sales. This downtrend says there’s more going on here than a lack of available homes for sale, however. Fewer-but-higher-priced home sales are carrying more than their fair share of the water.

New, Existing Home Sales Charts

Source: Census Bureau, National Association of Realtors, TradeStation

Last month’s new home sales will be posted on Tuesday of this week. Forecasts say we’ll see a slight pullback in the growth effort evident here as well.

Everything else is on the grid.

Economic Calendar

Source: Briefing.com

Real estate remains a focal point this week. In addition to Tuesday’s new home sales numbers, on that same day we’re going to hear the FHFA Housing Price Index update for July, and the Case-Shiller Index for the same month. As you can see, both are climbing again, and are expected to continue doing so. Just keep in mind these only indicate average sale prices for sold units, and don’t reflect the sheer number of sales made… at least not directly. Indirectly, they still generally point to one measure of the real estate market’s health.

Home Price Charts

Source: FHFA, Standard & Poor’s, TradeStation

It’s also an important week for sentiment measures. The third and final look at the University of Michigan’s consumer sentiment measure will be released on Friday. That data follows Tuesday’s look at the Conference Board’s consumer confidence score for September. Both are likely to slide lower again falling August’s lulls. That’s not an encouraging clue for the market.

Consumer Sentiment Charts

Source: Conference Board, University of Michigan, TradeStation

We’ll also be getting the third and final look at Q2’s GDP growth figure on Thursday, though economists don’t think it changed from the previous estimate of 2.0%. That’s not a great growth rate, suggesting inflation is taking a slow, grinding toll on the economy.

Stock Market Index Analysis

Kaboom. The S&P 500 lost 2.8% of its value last week, logging its worst week since March, and then September of last year.

That in and of itself isn’t the end of the world. In fact, it was so bad, it’s arguably good. It primes the market for a big bounce. Just don’t count those chickens before they’re hatched. Last week was also so bad that all of the indices broke under key technical support levels.

Take the S&P 500 as an example. Not only did the index fall under its 100-day moving average line (gray) at 4377, but also broke under August’s low of 4334 (yellow, dashed).

S&P 500 Daily Chart, with VIX and Volume

Source: TradeNavigator

Also notice the volatility index (VIX) is finally starting to push up and off of a floor… at 12.6. That move is even easier to see on the weekly chart below. The scope of last week’s loss in the context of the weakness since late-July is also easier to make out on the weekly chart. Things changed.

S&P 500 Weekly Chart, with VIX and Volume

ource: TradeNavigator

Even so, as much as things may have changed, it wasn’t enough to completely break the uptrend. This pullback so far only unwinds part of an overheated rally between May and July. The long-term uptrend is still intact. The lower boundary of that advance is at 4207, where the 200-day moving average line (green) and the straight-line support that connects the key lows since last October (light blue, dashed). That’s the support that really matters the most right now.

The Dow Jones Industrial Average broke below it’s key technical floor this past week as well — the lower boundary of a rising, converging wedge (framed by dashed lines on the daily chart). This shape followed by this breakdown usually portends a more serious setback… similar to carrying a rock up a ladder to drop it from an even-higher height.

Dow Jones Industrial Average Daily Chart

Source: TradeNavigator

The one index that didn’t slip into too much trouble? Incredibly enough, despite losing more ground than any other index (-3.6%), it’s the NASDAQ Composite. Although it too tumbled below its 100-day moving average line (gray) at 13,533, its selling stopped at 13,135. That’s where the index made a near-term low last month, but curiously, that’s also were the index peaked in August of last year. Clearly there’s something about that level.

NASDAQ Composite Weekly Chart, with VXN

Source: TradeNavigator

Even so, the market’s on the defensive here. Thanks to last week’s selloff it’s become clear that not only is the market vulnerable here, but it doesn’t actually take bad news to up-end stocks. It’s just that traders seem ready to interpret any news in the worst possible light. Between that mindset and the fact that all of the volatility indices are now starting to inch their way higher, everyone should at least prepare for more downside.

Also don’t be too quick to jump on any bullish effort early this week. We may well see it. But, it may also only be a response to the sheer depth of last week’s loss.

Thanks,

Price Headley

{kind=link}

Recent Comments