From Price Headley, BigTrends.com

For the first time in several weeks the market suffered a major weekly loss. When all was said and done the S&P 500 fell 2.2% last week. The rally underway since March hasn’t yet been officially broken. But, there are red flags now waving. Both the NASDAQ Composite and the S&P 500 waving them too.

We’ll look at why last week is so problematic in a moment, in conjunction with our look at how the market could still escape this brewing technical trouble. First, however, let’s run through last week’s most important economic news and then preview what’s in the lineup for this week.

Economic Data Analysis

Last week was pretty well loaded with economic news. But, there were only a couple of data sets we were really interested in.

The first of this is July’s ISM data from the Institute of Supply Management. The manufacturing measure ticked a little higher, but didn’t live up to expectations. The services measure, meanwhile, continued to fall even more than expected. In both cases the numbers remain in bigger-picture downtrends that should be of concern to long-term investors.

ISM Services and Manufacturing Index Charts

Source: Institute of Supply Management, TradeStation

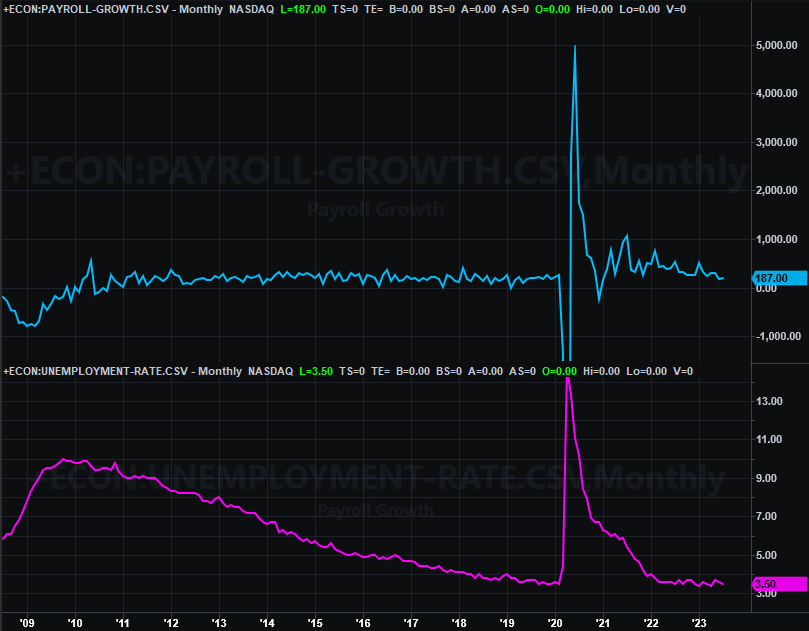

The only other economic news from last week worth mentioning is a biggie… July’s jobs report. Payroll growth of 187,000 fell short of the expected 200,000, and June’s initial guesstimate of 209,000 was actually dialed back to 185,000 new jobs. Nevertheless, the unemployment rate slipped back to 3.5%.

Payroll Growth and Unemployment Rate Charts

Source: Bureau of Labor Statistics, TradeStation

Some pundits were bearish on the disappointing payroll growth number. Keep things in perspective though. Unemployment is almost at a multi-decade low. There are few people left to step into open positions. Consumers are making relatively good money with their current jobs too, if recent spending reports are any indication.

Everything else is on the grid.

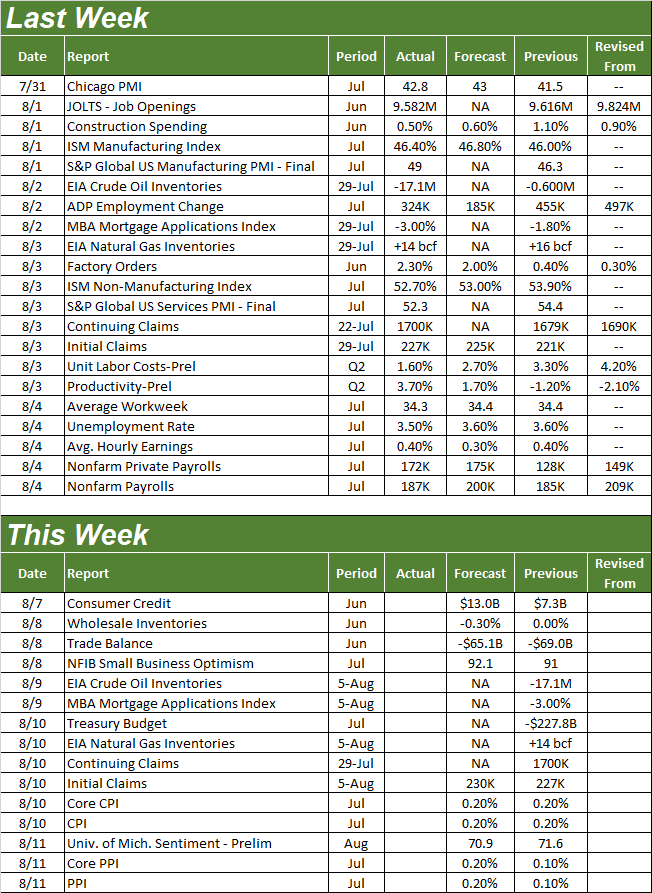

Economic Calendar

Source: Briefing.com

As the table above shows, several announcements are in the cards for this week. There’s only one set we really care about though. That’s the inflation data through last month. Consumer inflation numbers are due on Thursday. On Friday we’ll get the latest producer inflation report. All of them have been falling in earnest of late… producers’ costs more so than consumers. Although the pace of slowdown is expected to have slowed down in July, we’re still moving in a healthy direction.

Inflation Rate (Annualized) Charts

Source: Bureau of Labor Statistics, TradeStation

The inflation numbers have the potential to move the market as they may ultimately determine how aggressive the Federal Reserve has to be — or has to remain — with its interest rate increases.

Stock Market Index Analysis

We start this week’s analysis with a look at the weekly chart of the S&P 500… mostly for perspective. The point and purpose is to show you just how big the pullback was. It was the biggest weekly pullback since the one in early March, of course set the stage for an even bigger rally. This time though, the index is being asked to rekindle the rally with the disadvantage of still being overbought.

S&P 500 Weekly Chart, with VIX and Volume

Source: TradeNavigator

And the NASDAQ Composite’s weekly chart looks about the same, although arguably a little more bearish by virtue of more bearish volume. In fact, we’ve seen above-average volume behind the two weekly losses suffered in the last three weeks.

NASDAQ Composite Weekly Chart, with VXN and Volume

Source: TradeNavigator

Notice that both volatility indices — the VIX and the VXN — made measurable efforts to push up and off of their technical floors as well. This could be the start of something more significant.

Underscoring this possibility are a couple of details only evident on the daily chart of the S&P 500 and the NASDAQ Composite… although they’re the same basic red flag. That is, for the first time since April the NASDAQ is closing below its 20-day moving average line (blue). With that same stumble, the index is also now trading below a couple of different straight-line support lines (dashed red and yellow). Something’s clearly changed.

NASDAQ Composite Daily Chart, with VXN

Source: TradeNavigator

The S&P 500 hasn’t yet snapped any straight-line support. As was noted though, it is now below its 20-day moving average line (blue). The next major support level is near 4417, where the 50-day moving average line (purple) is converging with another line connecting the key lows from March and May (light blue, dashed).

S&P 500 Daily Chart, with VIX and Volume

Source: TradeNavigator

Conclusions? There’s no denying last week was rough. But, even the sizeable stumble hasn’t yet threatened the overall uptrend. Given the scope of the rally since March, we can still safely call it just a little predictable profit-taking. More may even be in store before all is said and done.

Nevertheless, it would be unwise to pretend this isn’t what corrections look like when they get going. There’s always the possibility this could be what last week was. We’re certainly in a time of year when stocks struggle, and we’re entering that period this year well overbought. That works against the market.

The key here may actually, ultimately be the volatility indices. They both moved higher last week, as could be expected when stocks are falling. Neither has begun a full-blown uptrend though. Given that both the VXN and the VIX are now coming off of major multi-year lows, their potential for a prolonged rise is higher here than it’s been in the past, with investors’ confidence unraveling in more serious way than it has of late. We’re looking for something more like we saw in early 2022, when the bear market first got going. Anything less than that and we can remain confident that even meaningful selling is just a temporary bear market correction.

Just keep your eyes on the 50-day moving average lines, which are purple on both of the daily charts above.

Price Headley,

BigTrends.com

{kind=link}

Recent Comments